Seven rules to optimize the management of your funds

source MSN / our comments in redIntroduction To build your equity portfolio it is better to stick to certain rules of prudence and common sense! To secure as far as possible, operation and ... to obtain, ultimately, the greatest benefit.

Defining your risk aversion

Defining your risk aversion returns to determine the proportion of shares that can hold in its portfolio. An important point in that, if answered objectively the investor will not panic in case of market decline and did not sell at the lowest ... after buying the highest. For some professionals, the proportion of shares to hold is that an investor can lose without recording a decline in living standards. In other words, should be invested only the money that we do not need a long time. For others it is determined by subtracting the number 100 in the age of the investor (40% for a saving of 60 years, 50% for a saving of 50 years, etc..). Investors who are unable (or unwilling) to define their risk aversion to leave their banks with the task of proposing several asset allocations, each characterized by a profile management more or less offensive. Generally, three profiles are available: Conservative, Balanced, Dynamic. The first is composed primarily of money market securities and bonds. Second, bonds and shares for a roughly equal share. The third profile (the more offensive) is predominantly composed of actions. Attention, depending on the school, the words "Caution", "Balance" and "Dynamic" do not have the same meaning. So it is almost impossible to compare with eg the performance of two funds "prudence".Investing medium to long term

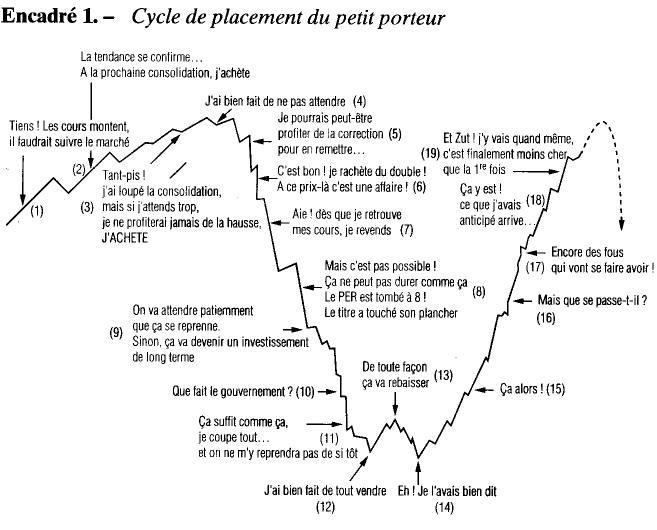

The best remedy for volatility. One example among many: in 1998, the Russian crisis and its monetary consequences in early summer, scariest and international markets are suddenly dropping broad market indices. The ACC is not immune to the movement. An investor who would buy an index Sicav 1 August 1998 would have seen the value of his fund to lose more than 27% two months later. Yet three years later, on 1 August 2001, the gain recorded by the same fund had reached 21.74% and this, despite the bursting of the bubble Internet (which brought down the ACC by 14% during the first eight months of the year 2001). Certainly, the magnitude of a crisis that has continued into 2002, our investor would, at the end of this year, the performance of its unit trusts back into the red. However, we easily measure the phenomenon of smoothing erratic market movements than the years it can achieve. Generally, investments in equities are the most efficient, provided them enough time. A study by the Credit du Nord between 1950 and 2000 on the average performance of three classes of assets that are money market securities, bonds and equities has thus demonstrated that the first reported each year, 8.2%, 9.5% the second and third 15.4%. But beware of the forty years of observation, maximum performance and minimum recorded by the assets have been substantially different. For money market securities, they were respectively 18.4% and 2.7%. For bonds, 33.2% - 9.7% and finally, for the shares, and 92.4% - 43.8%! Better to set a horizon of medium to long term to smooth the inevitable declines with periods of rising markets. Look this graph: the psychology of investors called "small carrier"

Stay invested whatever happens

The past year has been characterized by very high volatility. These parts of yo-yo markets are a bit like airplane turbulence: unpleasant but not dangerous and, anyway, inevitable for anyone who wants to go far. A survey by the management company Fidelity Investments, France has demonstrated that an individual would have remained invested in the French market between December 31, 1987 and December 31 2000 would, by considering the evolution of ACC, earned an annualized return of 17.9%. But if he had missed the ten best days recorded by the Exchange during that period, his performance would have fallen to 13.5%. Worse, it would have increased to 5.2% if he had missed the forty best sessions. Or, in thirteen years, a decline in performance around 70%! Much to the rounded back when markets go bad, rather than going out at the wrong time. Especially as the best and worst days are often close to each other. In addition, the days of sharp rises or declines very strong are not grouped on one or two particular years, but over several years of observation, for three or four days a year.interest (if any) investment programmed

The method we prefer -> no need to worry about changing course, choose the appropriate "nags" and just checking out all the quarters they behave properly. We'll cover this in Part 3.For many years, banks provide a mechanism of programmed investment in stock to buy each month, shares of unit trusts or mutual fund investment whose value has been divided so that the savings be paid immediately and fully vested. By this method, when the value of the shares in question is decreasing, the amount invested can acquire more. And when their value rises, the portfolio is valued even more quickly. In a period where markets are distinguished by high volatility, this mechanism allows the investor to lower the average purchase price of the shares. Of course, to be really interesting, the mechanism of payments scheduled to allow the investor to invest each month all of his stake. In other words, the amount of shares should have been divided into thousandths of a share. Where appropriate, this leads to broken which will be invested until the following month. Where a shortfall if the markets were up.

In addition, the method is well suited scheduled payments for periods when markets fall then fly. Otherwise, or, in general, when prices are in a phase of steady growth, an investment at a given date always gives, at the end of the period, better results.

It is difficult to oppose two formulas. A planned investment is an act of regular savings. An investment is realized once more come into some money outstanding (inheritance, for example). Attention in the latter case, not to invest on a short-lived peak, the managers recommend investing in three or four times a semester gap between operations. However, interest on investments depends largely on the period. A study published by INSEE in early 2003 has thus calculated the average performance of different assets depending on the time of placement and that of its liquidation.

INSEE considered, for example, if an investor who saved regularly throughout a decade prior to liquidate its investment over the next ten years. Assuming that he had invested in shares in the 80's and had liquidated its portfolio in the 90s, the average performance of its investment stood at 11%.

However, having done the same operation by placing in the 60 to recover its development during the 70s, our investor would have experienced a loss of 1% ... Small consolation, a bond investment was not more efficient in the first case (9% per annum) and slightly better in the second (1% per year). We practice this method across multiple life-support: every month, we invest the same amount, regardless of market developments. Objective: retirement!

Diversify management methods

There are different management styles offering a degree of complementarity. There are essentially management croissance (growth) the management value (undervalued) and index management. The first focuses on stocks with good earnings visibility ahead and giving hope and high earnings. This is the case of securities of the new economy, for example, whose recent journey resembles a roller coaster. For its part, the management value is for a manager to buy securities whose value is temporarily distressed, and to sell when it rises and crosses a threshold corresponding to its "true" value. In terms of performance, these funds do not show results as high as funds composed of growth stocks in the upward phase of the market. However, structurally, the funds managed by the method value are more resistant to falling markets and are characterized by volatility relatively low. Since the early 2000s, they often held the top spots. Lastmanagement type: index management. This category has recently expanded with the introduction in 2001, trackers. Like index funds, these securities are designed to replicate the performance of a large index (CAC, Eurostoxx, etc..). They usually represent a tenth or a hundredth of the value of the basket index in question and are continuously quoted, as an action (as opposed to index funds). In addition, ETFs are traded without rights of entry or exit fees and feature fees management low (0.5%). These products reflect the behavior of markets in the long term, always appear on the rise. They deny, however, the subscriber of the qualities of the manager to beat the benchmark, even though the same way, they avoid the consequences of his errors! Remains to be seen what weight to attach to each mode of management in its portfolio. Invest 50% of the funds of funds comprised of growth stocks, 40% of the value fund and 10% in securities that replicate the index must allow to enjoy the dynamic markets without taking excessive risks. We are followers of management value, through funding from Tocqueville, Admiral Management, ... our "nags"!

However, one can overlook the management "benchmarked" the SICAV "liners" of large institutions. Indeed, not to lose customers, banks require their managers to follow very closely the developments of a large index (or benchmark). That way, if the benchmark down - and the performance of the fund as well - responsibility lies with the behavior of markets and not to possible mismanagement of the company. What to reassure savers! Only problem: for performance finally close to those of the index, you have to pay management fees twice a Sicav quad index and a tracker!

In another type, it is now possible to include, as a diversification in its portfolio of hedge funds. In principle, this type of management is "uncorrelated" to changing markets (hence the success these past two years!). Result, many hedge funds managed to post positive results while financial markets are in the red. The funds for the general public mainly belong to the category of "enhanced cash" or "dynamic +". But their goal is to serve as performance generally equal to the rate of EONIA + 100 to 200 basis points (4 to 5% approximately), they are rather interesting.

Other hedge funds exhibit higher goals. In this case, it is better to prefer a fund of funds structure certainly more expensive but less risky costs due to the presence of various technical alternatives to the fund. Fund of funds means that you buy a fund that buys funds. Attention to the stack costs.

0 comments:

Post a Comment